Key Points:

Indonesia, a country blessed with vast amount of resources, is benefitting from rising commodity prices and strong external demand. However, has the market fully priced in the upside potential of the Jakarta Composite Index (JCI) after years of encouraging performance? Is the mining sector boom a convincing reason to invest in the country now? Resource Rich Nation

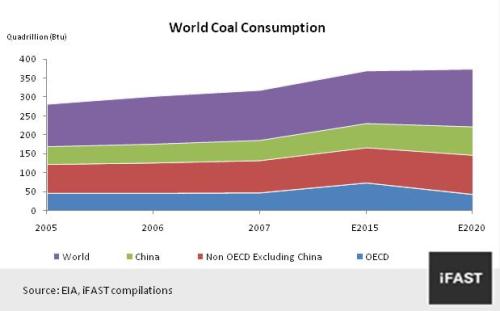

Indonesia is rich in non-renewable energy (coal), renewable energy (geothermal power), and agricultural products (palm oil, cocoa and rubber). It holds the title of the world’s largest thermal coal exporter, accounting for 26% of the world’s export. Besides that, Indonesia is also the world’s largest producer of natural rubber and palm oil. It’s cocoa production is ranked second in the world. Resource Demand Over the years, the growth momentum in the mining and agriculture industry was underpinned by the favourable demand prospects. Demand is expected to trend upward as the pace of industrialisation and urbanisation quickens in developing nations. Coal (41%) currently is the main source of electricity generation in the world, followed by gas (15.9%) and hydropower (15.9%). In 2009, China alone accounted of 46.9% of global coal consumption according to the BP Statistical Review of World Energy June 2010. US Energy Information Administration (EIA) projected China to remain the single largest consumer. (Chart 1)

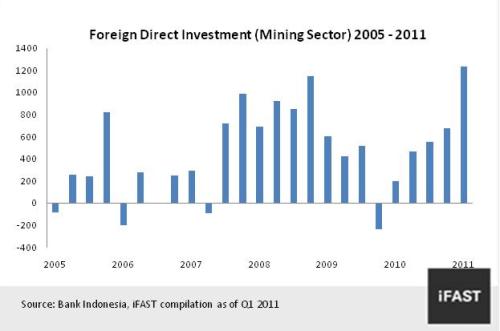

According to 2010 Economic Report on Indonesia, natural resource-based export has expanded to 52.7% of total export in 2010 from 50.3% in 2009. In addition, Indonesia’s non oil and gas export to China has grown significantly from 3.6% in 2000 to 10.8% in 2010. The growing demand for coal and other resources especially from China is important to the growth of Indonesia economy. Foreign Direct Investment Surge in Mining Sector The foreign inflow mainly goes into the mining industry to take advantage of the resource boom accounting for 28% of the total Foreign Direct Investment (FDI) in Q1 2011. The FDI remained in positive territory (net inflow) in 20 of 25 past quarters. Q1 2011 saw inflows of USD 1,237 million which surpassed the previous high of USD 1,148 million in Q4 2008. Going forward, we believe that the global demand of energy resources will not be as strong as previous quarters as the pace of world economic growth declines.

Resource Weight on Jakarta Composite Index Resource based (agriculture, mining, oil and gas) companies carry 23.99% weight in the Jakarta Composite Index (JCI) on the free floating market capitalization basis as of 6 September 2011. Resource sector emerged as the second sector in JCI, marginally behind financials (27.59%) but ahead of consumer sector (20.63%).

The mining sector (comprises 35 companies) of which 15 companies are coal related companies, 13 are involved in other minerals and precious metals and 7 are in the iron and steel industry. Table 1 below shows the breakdown of the resource sector into mining, agriculture and oil and gas sub-sectors. Table 1: Resource Weight on Jakarta Composite Index

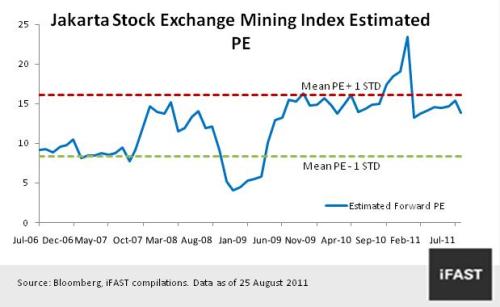

Valuation Despite the outlook of resource remain positive, we believe that the potential upside for the mining sector is limited. In Chart 4 below, we have compared the 12-month forward PE (blue live) against a range defined by the +1 standard deviation (red line) and -1 standard deviation of its average past over the past 5 years. As of 23 August 2011, the PE is 13.81X which is within the upper band of its historical average.

Turning to the JCI, its current PE is 15.1X (as of 25 August 2011), bearing in mind that we value fair PE level at 15X. Similarly, the closing price of JCI on 25 August 2011 is 3847, which is well above our target level of (3806 points) by end 2011. The JCI is the only index that is trading above its fair value under our coverage presently. Table 2: JCI Estimated Forward PE and Earnings Growth

| ||||||||||||||||||||||||||||||||||||||||||

CONCLUSION

The story of rising commodity prices and its inducement to Indonesia’s economy is losing its appeal as we see that valuation are relatively high and that demand will decline commensurately with the global economic growth. As such, we maintain a 2.5 stars ‘’Neutral’’ rating for Indonesia under our Star Rating.

Related Article

Looking Past The Current Turmoil – Upgrading 12 Markets; Downgrading Europe