Keypoints:

ISLAMIC FUNDS FOR EVERYONE - MUSLIMS AND NON-MUSLIMS

Many investors think that an Islamic fund is only suitable for Muslims as its investment strategy and criteria adheres to the Shariah (Islamic law). This is incorrect. Islamic funds are actually for everyone. The offering of Islamic fund in the asset management industry is meant to provide investors who wish to invest according to Shariah principles with a wide range of investment instruments which are Shariah-compliant. This also offers investors an alternative choice to conventional funds.

AUM (ASSETS UNDER MANAGEMENT) OF ISLAMIC FUNDS ARE GROWING

The growth in the global Islamic asset management industry (even during the 2008 financial crisis) over the past few years indicates that there is an increasing demand for Islamic funds. According to Ernst & Young’s Islamic Fund and Investment Report 2010, the Islamic fund industry is concentrated in the Gulf countries and Malaysia. Saudi Arabia is the largest Global Islamic Financial Hub in the world with total estimated Islamic AUM of USD22.7 billion and 174 Islamic funds, while Malaysia is the second largest with total estimated Islamic AUM of USD5.1 billion and 184 Islamic funds. With Islamic funds getting more and more popular in the global asset management industry, investors should not overlook them when making their investment decisions.

In this article, we drill deeper by looking into the stock screening process that identifies Shariah-compliant securities as well as comparisons between Islamic funds and conventional non-Islamic funds.

HOW ARE SHARIAH-COMPLIANT ASSETS IDENTIFIED?

A security is deemed as a Shariah-compliant security when it fulfills several Shariah criteria developed by the Shariah Supervisory Board for the stock screening process. In this part, we will discuss the stock screening process adopted by the Standard & Poor (S&P) Shariah Indices, Dow Jones Islamic Market (DJIM) Indices and the Securities Commission of Malaysia.

S&P SHARIAH INDICES AND DOW JONES ISLAMIC MARKET INDICES

There are two levels of screening for S&P Shariah Indices and DJIM Indices to remove securities that are not suitable for Islamic investment. The first is the sector-based screen to select companies with acceptable business activities. Companies with business activities related to Table 1 are screened out. According to DJIM Shariah Supervisory Board, a company classified “Financial” according to Industries Classification Benchmark (ICB) is considered eligible if the company is incorporated as an Islamic Financial Institution, i.e. Islamic Bank and Takaful Insurance Company. Real Estate companies are considered eligible if the company’s operations and properties are conducted in accordance with Shariah principles. After removing companies with unacceptable primary business activities, the companies are evaluated according to several financial ratios to remove companies with unacceptable levels of debts or impure interest income (refer to Table 2). This second accounting-based screen focuses on three factors – leverage, cash, and the share of revenue derived from unacceptable business activities.

| Table 1: Unacceptable business activities under Shariah principle | |

| S&P Shariah Indices | DJIM Indices |

| Pork • Alcohol • Gambling • Financials • Advertising and media (newspaper are allowed) • Pornography • Tobacco • Trading of gold and silver as cash on deferred basis |

• Pork-related products • Alcohol • Gambling • Conventional financial services (banking, insurance, etc.) • Entertainment (hotels, casinos, cinema, pornography, music, etc.) • Tobacco • Weapons and defense |

| Source: S&P Shariah Indices Methodology, Guide to the Dow Jones Islamic Market Indices | |

Table 2: Shariah-tolerable levels of debts or impure interest income |

||

| S&P Shariah Indices | DJIM Indices |

|

Leverage Compliance |

Debt / Market Value of Equity (12-month average) < 33 | Debt / Market Value of Equity (24-month average) < 33 % |

Cash Compliance |

•Accounts Receivables / Market value of Equity (12-month

average) < 49 % |

•(Cash + Interest Bearing Securities) / Market value of Equity (24-month average) <33 |

Revenue derived from unacceptable |

Revenues from unacceptable business activities are permissible, if: Income from unacceptable business activities other than interest income / Revenue < 5% |

Revenues from unacceptable business activities are permissible, if: Income from unacceptable business activities other than interest income / Revenue < 5% |

Source: S&P Shariah Indices Methodology, Guide to the Dow Jones Islamic Market Indices |

||

Table 3: Criteria for Shariah-complaint securities |

|

Core business activities |

Core business activities must not involve:

|

Source of income |

Income contribution from the following sources must not exceed 5% of total income and profit before tax

Income contribution from the following sources must not exceed 10% of total income and profit before tax

Income contribution from the following sources must not exceed 20% ototal income and profit before tax

Income contribution from the following sources must not exceed 25% of total income and profit before tax

|

Source: List of Shariah Compliant Securities by the Shariah Advisory Council of the Securities Commission Malaysia dated 26 November 2010 |

|

SECURITIES COMMISSION OF MALAYSIA[1]

In Bursa Malaysia, securities listed as Shariah compliant are evaluated by the Shariah Advisory Council (SAC) of the Securities Commission Malaysia in three areas.

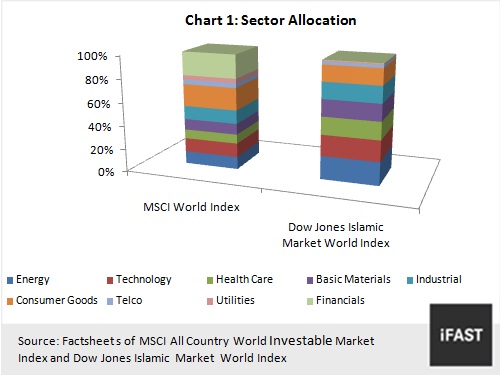

MSCI WORLD INDEX AND DOW JONES ISLAMIC MARKET WORLD INDEX

In order to have a clearer comparison of how Islamic funds stack up against conventional non-Islamic funds, we compare the MSCI World Index and Dow Jones Islamic Market World Index. Unlike the MSCI World Index, the Dow Jones Islamic Market World Index only allocates a marginal 0.25% of its market capitalisation into the financial sector, while MSCI World Index has 20.5% in this sector.

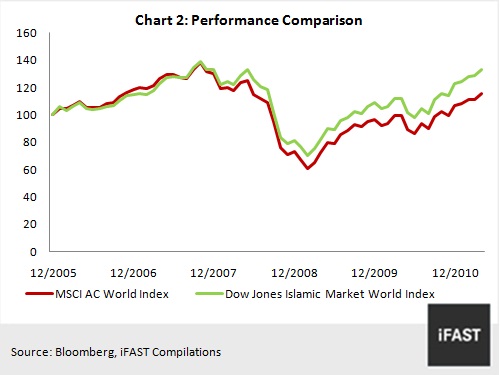

The Dow Jones Islamic Market World Index also has lower allocation on consumer goods, telecommunication and utilities sectors as compared to the MSCI World Index. Nonetheless, the Dow Jones Islamic Market World Index has much higher allocation in the energy, technology, health care, as well as basic materials and industrial sectors (refer to Chart 1). A common question is whether an Islamic equity fund will lag conventional equity funds because of their restrictions on Shariah noncompliant assets. However, this may not be the case. Chart 2 and Table 4 show that the Dow Jones Islamic Market World Index has consistently outperformed MSCI World Index since 2007 even though the index does not have much allocation in the financial sector.

During the 2008 financial crisis, the Dow Jones Islamic Market World Index was more resilient than the MSCI World Index, dropping by 38.9% compared to a 43.5% drop in MSCI World Index. While it declined less than the MSCI World Index, the Dow Jones Islamic Market World Index also performed better than the MSCI World Index during the recovery from 2009 to 2010. As of 29 April 2011, the Dow Jones Islamic Market World Index returned an 8.4% gain, which was higher than the 7.9% gain in the MSCI World Index.

Table 4: Performance comparison between MSCI World Index and Dow Jones Islamic Market World Index |

||||||

|

2006 |

2007 |

2008 |

2009 |

2010 |

YTD |

MSCI World |

18.8% |

9.6% |

-43.5% |

31.5% |

10.4% |

7.9% |

Dow Jones Islamic Market World |

14.5% |

16.4% |

-38.9% |

33.8% |

12.8% |

8.4% |

Source: Bloomberg, Fundsupermart compilations. Data as of 29 April 2011 |

||||||

CONCLUSION

During the 2008 financial crisis, Islamic equity funds were able to draw attention from investors as they proved more resilient than conventional equity funds. Incidentally, the global financial crisis in 2008 was partly the result of excessive leverage in the financial system and investment into exotic financial derivatives such as credit default swaps and collaterised debt obligations — all prohibited under Shariah principle.

Besides, Islamic equity funds usually have lower risk as compared to conventional equity funds. This is because Shariah-compliant securities have less leverage than Shariah non-compliant securities (based on the screening criteria of S&P and Dow Jones). In addition, Shariah principle prohibits Gharar, which means speculation is prohibited.

With more and more Islamic investment instruments being introduced, it will be beneficial for investors to equip themselves with the knowledge of Islamic investment instrument and basic Shariah principles. With better understanding, investors will be able take advantage of the unique features of Islamic funds and complement them with their overall portfolio.

Related Articles

An Investor's Guide To Islamic Funds

3 Funds Stand Out in Malaysia Islamic Equity Space

[1]. Reference from List of Shariah Compliant Securities by the Shariah Advisory Council of the Securities Commission Malaysia dated 26 November 2010 Yeoh Mei Kei is an analyst of iFAST Capital Sdn Bhd. |

| This article is not to be construed as an offer or solicitation for the subscription, purchase or sale of any fund. No investment decision should be taken without first viewing a fund's prospectus and if necessary, consulting with financial or other professional advisers. Any advice herein is made on a general basis and does not take into account the specific investment objectives of the specific person or group of persons. Past performance and any forecast is not necessarily indicative of the future or likely performance of the fund. The value of units and the income from them may fall as well as rise. Opinions expressed herein are subject to change without notice. Please read our disclaimer in the website. |

|